ESG Frameworks: ESG vs ESG Frameworks Explained

- Inemesit Ukpanah

- Jul 9

- 8 min read

Environmental, Social, and Governance is now central to how businesses talk about risk, impact and opportunity, but many people still treat “ESG” and “ESG frameworks” as if they are the same thing. They are not the same, and that confusion makes it harder for companies, especially SMEs, to choose the right ESG frameworks, meet real obligations and avoid wasted effort.

This article clearly explains the difference, connects ESG frameworks to the CSRD and ESRS landscape for SMEs, and shows how to use ESG as a strategic lens rather than a reporting shortcut.

Table of Content

ESG as a concept: the lens, not the rulebook

ESG stands for Environmental, Social, and Governance and describes the three major dimensions through which an organisation interacts with the world. It is a high-level lens for evaluating how your activities affect and are affected by climate, people and governance structures.

Under the environmental pillar, you look at topics such as energy use, emissions, waste, resource efficiency and pollution. Under the social pillar, you focus on workers, communities, customers and human rights, while governance covers leadership, board oversight, ethics and internal control.

The concept of ESG helps you ask structured questions. What are our biggest environmental risks? Which social issues could damage trust? How strong is our governance when something goes wrong? It does not tell you exactly how to measure every topic or how to format disclosures for external audiences.

For SMEs, this distinction matters. ESG, as a lens, is the starting point for operational change: renegotiating energy contracts, improving safety procedures, mapping supplier risks, and strengthening decision-making. Those decisions come before ESG reporting, not after.

ESG frameworks: the tools that structure reporting

ESG frameworks are structured systems that define what you report, how you organise the information and often which audience you serve. They exist so that investors, regulators, banks, and other stakeholders can read your ESG data consistently and comparably.

Frameworks provide principles and structure. Standards provide detailed metrics, definitions and disclosure requirements inside that structure. Together they govern how sustainability data is measured, reported and verified.

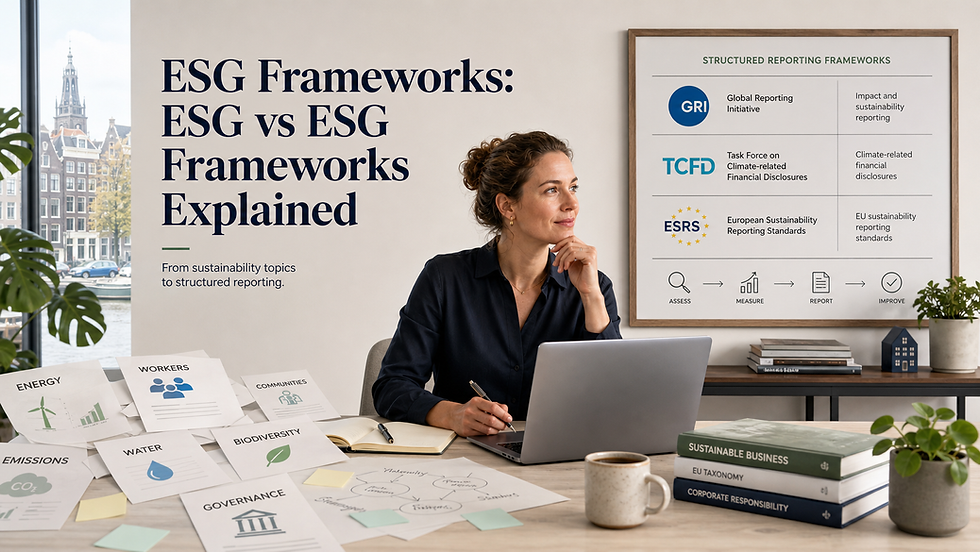

Common ESG frameworks and standards include:

Term | What it is | Main purpose | Typical users |

ESG (concept) | Overall sustainability lens | Identify risks, impacts and opportunities across E, S and G | Any organization or investor |

GRI | Reporting framework and standards | Broad impact-based sustainability reporting | Large firms and public entities |

SASB / ISSB | Reporting standards | Financially material ESG for investors and markets | Listed companies and capital providers |

TCFD | Disclosure recommendations | Climate-related financial risk disclosure | Financial sector and corporates |

ESRS / CSRD | Regulatory reporting standards | Mandatory EU corporate sustainability reporting | EU regulated and listed entities |

GRI focuses on how a company affects the environment, people and the economy and is widely used as a general sustainability reporting framework. SASB and ISSB focus on financially material information that could influence enterprise value and provide sector-specific metrics for investors.

TCFD is climate-specific. It structures disclosures around governance, strategy, risk management, metrics and targets for climate risks and opportunities and remains a core reference for banks and regulators. ESRS operationalises the CSRD in the European Union and links ESG topics to legal reporting requirements and to the concept of double materiality.

Each framework has a different scope, audience and regulatory status. Some are voluntary. Some are market-driven. Some are mandatory under law.

ESG vs ESG frameworks: different roles, different risks

Concept versus tool

ESG, as a concept, tells you which areas matter. ESG frameworks tell you how to report on those areas.

When a company says “we follow ESG”, that statement does not reveal whether it uses GRI, ESRS, ISSB or TCFD or whether it reports mainly impact information, financial risk information or climate only. The lack of precision can cause real problems when banks, investors or large customers expect alignment with specific frameworks.

For SMEs, this confusion often arises when a large client sends an ESRS-aligned or VSME-style questionnaire, while internal teams still speak in general terms about ESG. Without a clear distinction between concept and framework, it becomes hard to see which questions are discretionary and which reflect hard obligations.

Different audiences and obligations

Frameworks are designed for particular audiences and regulatory contexts. GRI speaks to broad stakeholder interests including communities and public authorities. SASB and ISSB focus on investors and capital markets, concentrating on financially material topics. TCFD focuses on climate risks and is driven by financial stability concerns. ESRS and CSRD serve EU regulators and assurance providers and create binding rules for in-scope companies.

Some frameworks remain voluntary for most companies, such as GRI and TCFD in many jurisdictions. Others are expected by investors even when not written into law, such as ISSB for global baseline disclosures. ESRS and CSRD are mandatory for large EU undertakings and listed SMEs that meet specific thresholds.

If you treat “ESG” and “ESG frameworks” as interchangeable, you blur the line between what is legally required, what is commercially expected and what is optional but strategically useful. That can lead SMEs to either over-report or under-comply.

Scope and materiality logic

Frameworks differ in scope. GRI and ESRS cover broad sustainability topics and consider environmental, social and governance impacts. TCFD is narrower in scope and focuses entirely on climate-related risks and governance. SASB and ISSB concentrate on sector-specific topics that affect enterprise value.

Frameworks also differ in how they define materiality. Impact materiality looks at how the company affects people, planet and the economy. Financial materiality looks at how sustainability issues affect the company’s cash flows and value. ESRS combines both perspectives in a double materiality approach, which is now central in EU corporate sustainability reporting.

If you speak only about “ESG”, you hide these differences. That can produce reports that omit important impact topics or fail to address the financial risk information investors and lenders expect.

Strategy versus disclosure

ESG, as a management lens, supports strategy, risk assessment, and opportunity mapping across operations and the value chain. ESG frameworks focus on structured disclosure and assurance to help external readers understand and compare your performance.

If an SME treats ESG only as a reporting exercise, it tends to jump straight to templates and dashboards before fixing the underlying decisions about energy, space, labour and suppliers. That sequence locks today’s inefficiencies into tomorrow’s report, making it harder to challenge them later.

If an SME uses ESG evidence as a concept first, it can begin with operational clarity and then select frameworks that align with its stakeholder landscape and capacity. Reporting then becomes a reflection of change rather than a cosmetic layer on top of existing habits.

ESG frameworks in the CSRD and ESRS context for SMEs

Corporate Sustainability Reporting Directive and European Sustainability Reporting Standards are changing how sustainability information flows through European value chains. Large undertakings and listed companies must publish reports on their environmental and social risks and on how their activities affect people and the environment.

For SMEs, the picture is more nuanced.

Listed SMEs on regulated European markets have direct reporting obligations once proportionate ESRS standards for listed SMEs come into force, using the LSME standard.

Non-listed SMEs and micro enterprises are not directly within the scope of the CSRD but face indirect pressure because large companies must report value chain information and therefore often request ESG data from suppliers.

EFRAG has developed proportionate ESRS for SMEs through VSME for voluntary reporting and LSME for listed SMEs so that smaller businesses can implement sustainability reporting in a practical and relevant way.

This has direct implications for ESG frameworks.

First, ESRS does not exist in isolation. It builds on and aligns with other frameworks and standards that many companies already use, such as GRI, TCFD and the global ISSB baseline.

Second, SME-specific standards like VSME translate the complexity of the ESRS into simpler, proportionate reporting structures that smaller businesses can handle.

Third, the CSRD framework explicitly recognises that information requests from large undertakings to SMEs should not exceed what SMEs are expected to disclose under their own standards, which limits the risk of disproportionate data demands.

For a Dutch SME, this means ESG frameworks are not just a theoretical choice. They sit within a structured system in which the ESRS and CSRD define legal expectations for large buyers, and VSME-style standards offer smaller suppliers a way to present relevant ESG information without adopting the full set of ESRS requirements.

A practical example: using ESG and frameworks in a Dutch SME

Imagine a mid-sized supplier in the Netherlands that serves several large EU manufacturers. Internally, the company uses ESG as a lens to map key risks and opportunities across its operations and value chain. It identifies energy waste in offices and warehouses, gaps in safety training and unclear escalation routes for governance issues.

Externally, the company sees that its largest client is preparing ESRS-compliant reporting under the CSRD and begins sending questionnaires referencing climate, social, and governance indicators consistent with ESRS topics. A bank begins asking for climate risk information aligned with TCFD-style disclosures as part of its lending criteria.

The SME now has to intelligently choose and combine ESG frameworks.

It adopts a simple sustainability reporting approach, based on GRI principles, to describe impacts on the environment, people, and the economy in language that stakeholders recognise.

It aligns climate disclosures with TCFD recommendations, enabling the bank to assess how governance, strategy, and risk management address climate-related risks.

It studies VSME guidance and ESRS data points related to its activities to make future questionnaires from big buyers easier to answer and more consistent.

Throughout, the company keeps ESG as the overarching management lens and treats GRI-, TCFD-, and ESRS-aligned tools as specific frameworks that address defined audiences and obligations. It does not simply say “we follow ESG.” It states clearly which frameworks it uses and why.

That clarity helps the SME avoid lengthy reports that no one reads, keeps effort proportionate to the work's size, and increases trust with buyers and lenders who see data presented in familiar structures.

How SMEs can work with ESG frameworks without losing sight of ESG

SMEs do not need to adopt every framework. They need to connect ESG as a lens to a small set of frameworks that match their context. A practical sequence can help.

Use ESG to map priorities. Identify environmental, social and governance topics that are most relevant to your operations, workforce and value chain. This map becomes the backbone of your sustainability strategy.

Identify which frameworks your stakeholders reference. Track whether banks mention TCFD or ISSB, whether major customers refer to ESRS or VSME, and whether any investors or partners signal GRI or other impact frameworks.

Classify frameworks by audience, scope and obligation. Mark which are regulatory, which are investor-driven and which are voluntary. Note whether they focus on broad impacts, climate only or financially material topics.

Choose a small combination of frameworks. Most SMEs benefit from a single, broad impact-narrative framework, such as GRI or a VSME-aligned approach, plus a climate framework such as TCFD or ISSB S2 if lenders expect it. ESRS datapoints then inform which questions to prepare for in supply chain reporting.

Communicate clearly. In your ESG statements, explain that ESG is your management lens and that you report in line with specified frameworks. This builds credibility and reduces confusion about what your reports actually show.

By making these distinctions explicit, SMEs keep ESG as a strategic compass and use frameworks as precise tools. They stop treating ESG and ESG frameworks as interchangeable and start using them as complementary parts of one system.

Comments