Sustainability reporting for small businesses

- Inemesit Ukpanah

- Mar 30

- 9 min read

Updated: Apr 1

You did not plan to become a sustainability reporter. Then a customer sent a questionnaire. Or your bank asked for ESG data before approving a loan. Or a landlord requested an environmental summary before renewing your lease.

Now you are here, reading about sustainability reporting, and you have no sustainability team.

This article explains what sustainability reporting actually means for a small business. It covers what the EU framework now requires from your clients, what you are actually being asked to produce, and how to build a credible response without hiring a consultant or learning a new framework from scratch.

Table of Content

Why do small businesses receive sustainability reporting requests

The VSME standard: what sustainability reporting looks like for a small business

What sustainability reporting does not mean for a small business

The frameworks behind sustainability reporting: what small businesses do not need to learn

What sustainability reporting requests can your clients legally ask for

What sustainability reporting means for a small business

Sustainability reporting is the practice of documenting and communicating a business’s environmental, social, and governance impacts. For large listed companies, it involves formal annual reports published to regulators and investors. For a small business, it means something far more practical.

Sustainability reporting is no longer reserved for large listed companies. With the rollout of the CSRD and its cascading effects across value chains, SMEs are increasingly asked to disclose their environmental, social, and governance practices.

That cascade lands in your inbox as a questionnaire. The questionnaire asks about your energy use, waste practices, employment policies, and governance structure. You do not need to publish a glossy report. You need to provide organised, documented answers with evidence attached.

Studies indicate that 78% of suppliers already receive sustainability requests from their clients. Most of those suppliers are small businesses with no sustainability infrastructure. The requests arrive regardless.

Why do small businesses receive sustainability reporting requests

The reason is regulatory. The EU Corporate Sustainability Reporting Directive (CSRD) requires large companies to report on their sustainability performance. That reporting includes data from their supply chains. When a large client reports, they need your data to complete their own disclosures.

The Omnibus I simplification package, adopted in February 2025, proposed reducing mandatory CSRD reporting to companies with more than 1,000 employees. For companies with up to 1,000 employees, the Commission proposed to adopt a voluntary reporting standard.

Under the EU Commission’s Omnibus proposals, approximately 80% of companies currently required to report under the CSRD will no longer be subject to the sustainability reporting obligation. The number of companies required to report is expected to decrease from approximately 45,000 to about 10,000 companies.

That sounds like good news for small businesses. It is, partially. The legal obligation falls away. The commercial pressure does not. Large clients still need supply chain data to complete their own reports. Banks still apply sustainability criteria to lending decisions. Landlords still ask for environmental data at lease renewal.

The value-chain cap protects smaller companies from excessive information requests. It prohibits companies in the scope of the CSRD from requesting information from other companies in their value chain above a certain limit. The VSME standard defines that limit. Understanding that standard tells you exactly what you need to prepare and what you can refuse.

The VSME standard: what sustainability reporting looks like for a small business

The VSME is a framework built specifically for small businesses facing sustainability reporting requests. The European Commission officially recommended its uptake on 30 July 2025, encouraging banks, investors, and large companies to base their ESG data requests on this standard, reducing confusion and compliance costs for smaller businesses.

Unlike the CSRD, which requires hundreds of data points, the VSME relies on around 60 ESG indicators in its Basic Module, roughly ten times fewer.

The Basic Module constitutes the entry level. It uses simplified language, includes 11 disclosure requirements covering key ESG indicators, and includes a streamlined narrative. All disclosures are required, but they apply only when relevant, to reduce the burden on the companies concerned.

A first VSME report can typically be produced within one to two weeks. It does not require a double materiality assessment. It does not require an external audit. It requires organised evidence and a short written summary.

The table below shows how the VSME Basic Module disclosure areas map to evidence that a small business already holds.

VSME Basic Module: what it asks for and what you already have

VSME disclosure | What it asks for | Evidence you likely already hold |

B1 General information | Business description, sector, employee count | Company registration, website about page |

B2 Governance | Who is responsible for sustainability | Director name, one-page policy statement |

B3 Energy and GHG emissions | Annual kWh consumption, Scope 1 and Scope 2 emissions | Utility invoices, gov emissions conversion factor |

B4 Pollution | Any significant pollution incidents | Health and safety records |

B5 Biodiversity | Any significant biodiversity impact | Site description, relevant only if applicable |

B6 Water | Annual water consumption | Sub-meter readings or utility invoices |

B7 Waste | Waste volumes and separation approach | Waste contractor invoices and collection records |

B8 Own workforce | Employment conditions, pay equity, health and safety | Employment contracts, H+S policy, training records |

B9 Value chain workers | Any labour concerns in your supply chain | Supplier code of conduct |

B10 Communities | Any significant community impact | Relevant only if applicable |

B11 Business conduct | Anti-bribery and data protection | GDPR privacy policy, anti-bribery clause |

Most of this evidence already exists inside your business. It sits in utility invoices, HR files, and legal documents. It has never been organised for sustainability reporting purposes. That is the only problem to solve.

Greennect provides a downloadable evidence folder template built specifically for small teams completing their first VSME-aligned evidence file.

What sustainability reporting does not mean for a small business

Three common misunderstandings waste time and money.

It does not mean publishing an annual sustainability report. Large companies publish public sustainability reports because regulators and investors require them. No external party requires that from a small business. You need a document you can share on request. A two-page ESG summary serves most client, bank, and landlord requests.

It does not mean achieving carbon neutrality first. The VSME does not ask whether you have reached net zero. It asks what your current energy use is and whether you track it. Reporting your current position honestly scores better than reporting nothing while you wait to have something impressive.

It does not mean hiring a sustainability consultant before you start. The most common data gaps in VSME reporting are a missing environmental policy statement, a missing supplier code of conduct, and an untranslated energy figure. Each takes under two hours to resolve. The five-step ESG data collection process explains how to address those gaps systematically.

How sustainability reporting differs by business type

The VSME applies across all sectors. The practical starting point differs.

Office-based businesses face the most straightforward version of VSME reporting. Their primary environmental data points are energy consumption and waste. Water consumption is usually modest. Scope 1 emissions are minimal unless the business operates company vehicles. The green office habits article covers which daily practices generate trackable ESG evidence and which ones produce no reporting value.

Co-working spaces and flex office tenants face a specific problem. They cannot control building-level energy data. The landlord holds it. The co-working ESG audit article explains how tenants request and document that data when it is not provided automatically.

Service businesses with supply chains need to pay closer attention to B9 (value chain workers) and B11 (business conduct). A supplier code of conduct and a basic anti-bribery policy resolve both disclosures. Without them, those VSME fields go blank.

Manufacturers and logistics companies face more demanding environmental disclosures. Their energy use is higher, Scope 1 emissions are significant, and waste volumes are larger. The ESG compliance guidelines article covers the starting point for those sectors.

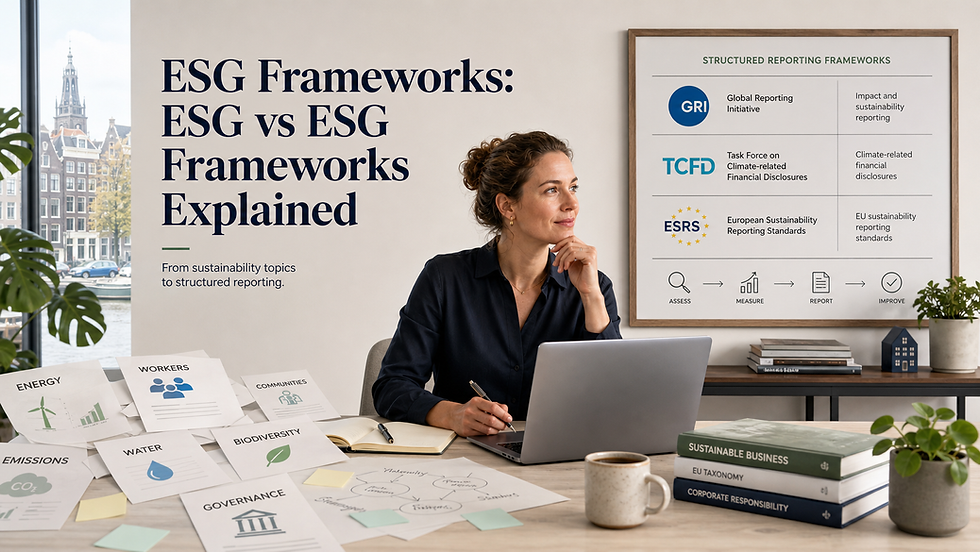

The frameworks behind sustainability reporting: what small businesses do not need to learn

Several sustainability reporting frameworks exist. Most are irrelevant to small businesses operating outside the CSRD’s direct scope.

GRI, the Global Reporting Initiative, produces the world’s most widely used sustainability reporting standards. Its audience is large organisations with dedicated sustainability teams.

EFRAG’s VSME standard is the relevant framework for non-listed small businesses in Europe. It does not require GRI literacy. It uses plain language and an “if applicable” principle.

The EU Commission’s official Q&A on the VSME recommendation explains the relationship between the VSME, the Omnibus package, and the value-chain cap in direct terms. It is worth reading once before starting any VSME preparation.

KPMG’s analysis of the VSME standard examines how the standard interacts with the CSRD requirements for businesses operating in the supply chains of large companies.

The VSME is the only framework a small business without a sustainability team needs to understand. Everything else is context.

What sustainability reporting requests can your clients legally ask for

This matters. Since February 2026, the EU Omnibus Package has been in force. The value-chain cap prohibits companies subject to the CSRD from requesting information from other companies in their value chain above a certain limit. This voluntary standard defines what information companies in scope of the CSRD can reasonably request from companies outside the CSRD scope.

The VSME Basic Module sets that limit. If a client sends a questionnaire that asks for information beyond the 11 VSME disclosure areas, you can reference the VSME recommendation and request that the scope be reduced. This is not an aggressive position. It is legally supported.

Greennect covers how to answer a supplier sustainability questionnaire in full, including which sections you can challenge and how to frame a credible response without specialist help.

How to start sustainability reporting this week

The starting point is not a framework. It is an inventory.

Spend two hours pulling together the documents that already exist in your business. Pull the last three utility invoices and note the kilowatt-hour totals. Pull your most recent waste contractor invoice. Pull your employment contract template and your GDPR privacy policy. Check whether a health and safety policy exists in written form.

That exercise reveals two things. First, how much VSME evidence do you already hold? Second, which of the three common gaps do you need to close: an environmental policy statement, a supplier code of conduct, or an energy-to-emissions conversion? The EFRAG SME sustainability reporting hub publishes worked examples and supporting materials for businesses completing their first VSME disclosure.

The VSME standard explained covers each gap and how long it takes to close. Most small businesses can answer most VSME Basic Module disclosures within one week using documents they already have.

A 20-minute introductory call with Greennect maps, which specific disclosures apply to your business, and which evidence is missing. No preparation is needed before that call.

FAQ: Sustainability reporting for small businesses

What is sustainability reporting for small businesses?

Sustainability reporting for small businesses is the practice of documenting environmental, social, and governance data and providing it on request to clients, banks, or landlords. It does not require a formal published report. The EU's VSME Basic Module defines 11 disclosure areas that cover most requests a small business receives. Most of the required evidence already exists inside the business in the form of utility invoices, employment contracts, and policy documents. The gap is organisation, not the absence of data.

Do small businesses have to produce sustainability reports?

Small businesses with fewer than 1,000 employees are not legally obligated to produce sustainability reports under the EU Omnibus Package, which has been in force since February 2026. The commercial obligation is different. Large clients subject to CSRD need supply chain data. Banks apply sustainability criteria to lending. The EU value-chain cap limits what clients can request from small suppliers to the scope defined by the VSME standard. Understanding the scope tells you what to prepare and what to decline.

What does a sustainability report for a small business include?

A VSME-aligned sustainability summary for a small business covers general company information, governance structure, energy and greenhouse gas emissions, water use, waste management, employment conditions, supply chain conduct, and business ethics. For most small office-based businesses, the practical output is a two-page ESG summary with an attached evidence folder. That folder contains utility invoices, employment contracts, a health and safety policy, a supplier code of conduct, a GDPR privacy policy, and a one-page environmental policy statement.

How long does sustainability reporting take for a small business?

A first VSME-aligned sustainability report takes one to two weeks for a small business starting from scratch. Most of that time is spent gathering existing documents, not creating new ones. Writing missing policies takes under four hours in total. Converting energy figures to emissions estimates using the UK government's free conversion factors takes one hour. A second report takes considerably less time because the evidence folder already exists.

Who is required to do sustainability reporting?

Under the EU Omnibus Package adopted in February 2026, mandatory sustainability reporting under the CSRD applies only to companies with more than 1,000 employees. Small businesses below that threshold face no legal obligation to publish a sustainability report. The commercial obligation is different. Large companies subject to the CSRD are required to request sustainability data from their suppliers to complete their own disclosures. The VSME standard sets the ceiling on what large companies can request from smaller suppliers. Small businesses use the VSME Basic Module to respond to those requests, not CSRD.

Comments